Background

What is the archetype and What is its purpose?

The archetype…

…describes essential steps of the energy transition

The energy transition archetype describes and illustrates the required changes to the energy system over time to move from a currently largely fossil fuel-based system towards a clean, affordable and sustainable system based on flexible and decentralised renewable energy sources. It thus describes the essential steps of the energy transition by considering its different dimensions including aspects such as infrastructure and technology, policy and markets, as well as broader social implications. Whilst using the broader term “energy transitions,” the archetype reflects the focus of the CASE programme and centres predominately on the power sector.

…is a generic conceptual framework

The archetype is meant as a generic conceptual framework which describes the power sector transition in general terms applicable to all countries and regions. At the same time, it takes account of the fact that transition pathways, in particular in terms of speed and starting point, can be very different depending on the specific circumstances and characteristics of the country. The country-specific application of the archetype is implemented through the power sector tracking tool, which is being developed in parallel and which will allow stakeholders to assess country specific progress of the transition along a set of key indicators.

…reflects joint understanding of CASE members

The archetype reflects the CASE members’ joint understanding of what we mean when we speak about the “energy transition in the power sector” in Southeast Asia. It serves the purpose of helping the consortium members to align and be clear about the joint vision and common goal in order to define activities in a targeted and strategic way. In addition to providing the conceptual framework for enabling the tracking of progress of the energy transition in each country, it aims to provide a useful basis for discussion and dialogue with all stakeholders directly working on the energy transition in the region as well as the wider public.

…has been developed by CASE members

The archetype has been developed in a consultative process between the CASE consortium members. It is the result of various discussions among the different partners taking into account the different perspectives on the future vision of the power sector from the international, climate policy and national perspectives.

Approach

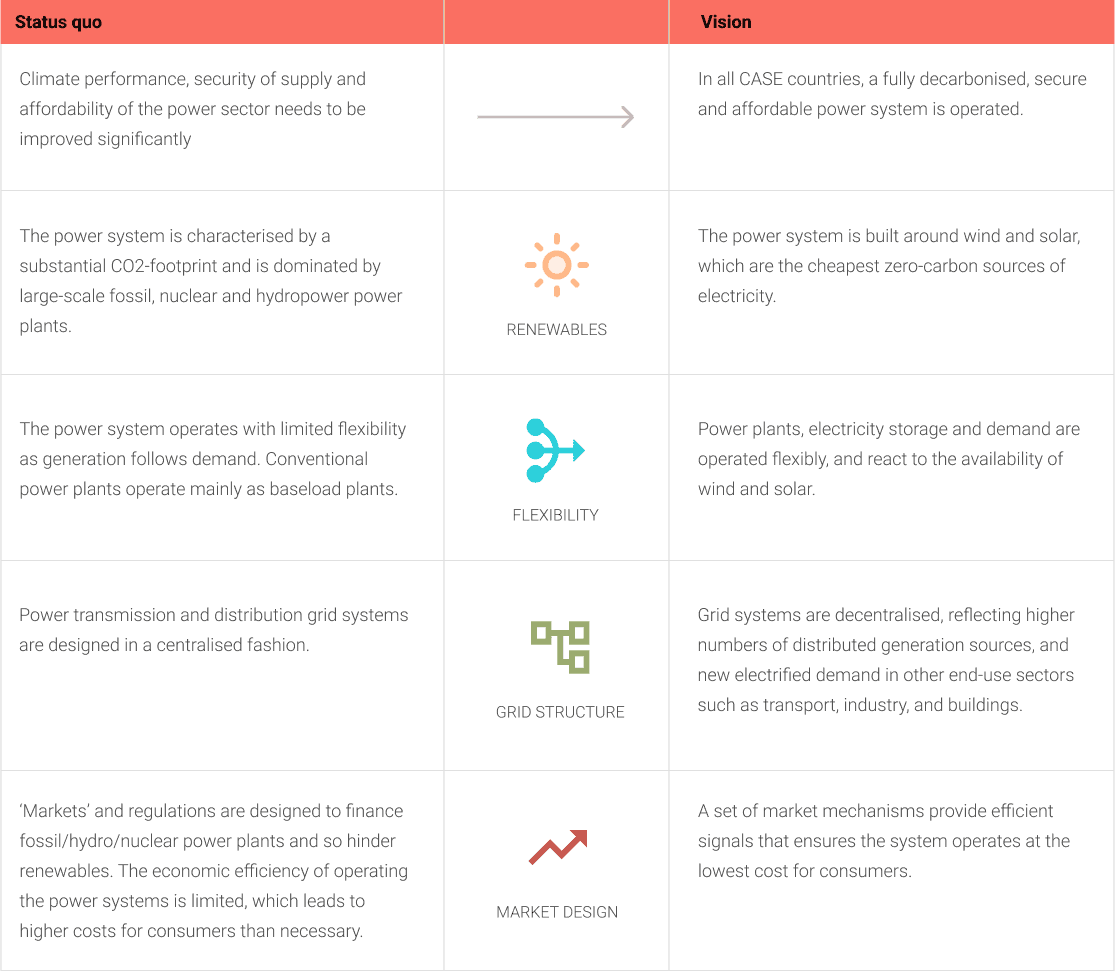

From status quo to long term vision

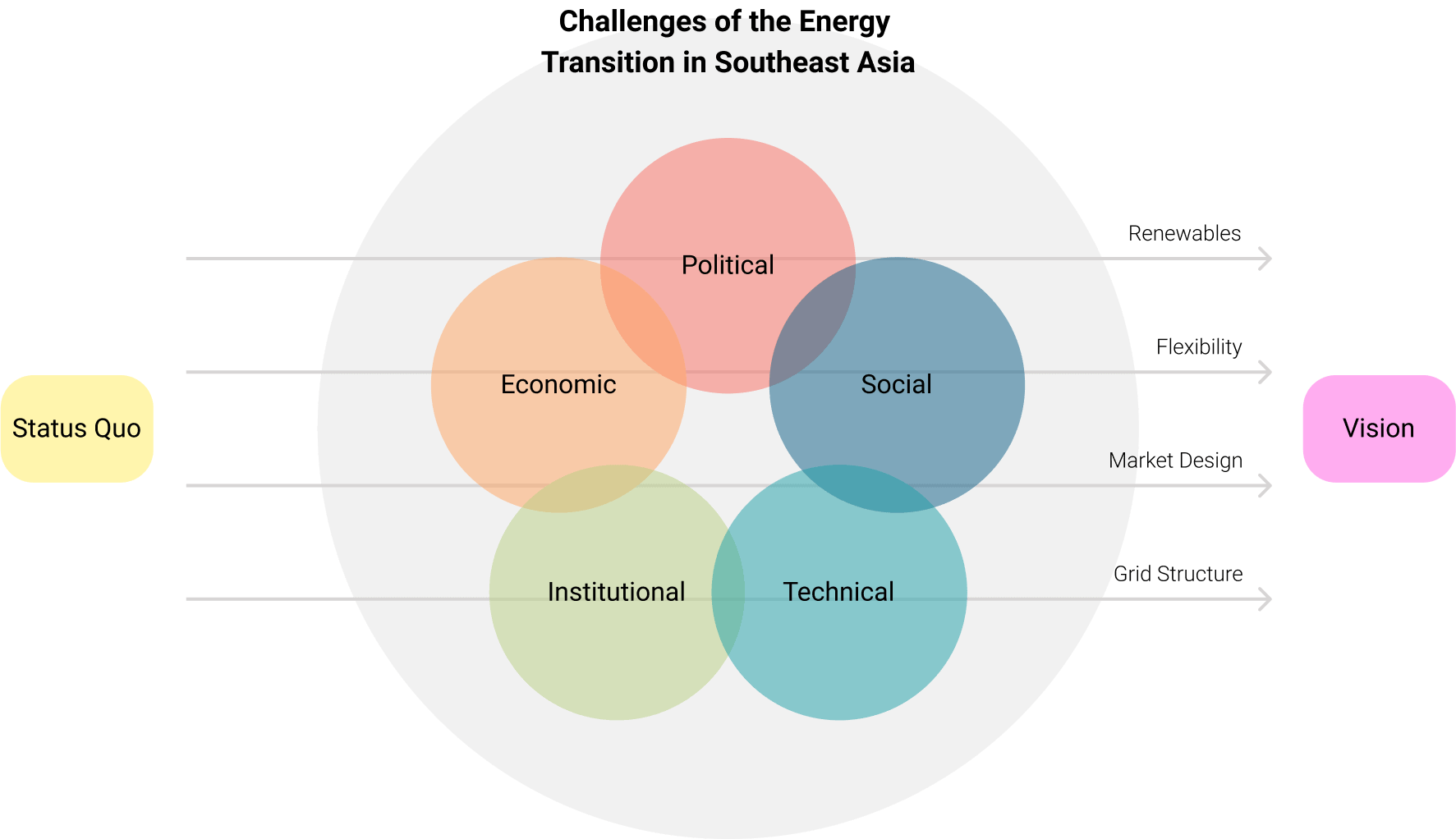

The archetype defines four key elements of the power sector transition and the vision of their future state: technologies, flexibility, market design and grid structure. In order to achieve this vision, a range of challenges need to be addressed and overcome. The challenges are generic in the sense that they may be present to varying degrees according to country contexts.

The archetype describes each of these challenges as a way to help stakeholders understand where interventions and actions may be needed to accelerate the move towards a clean, affordable and sustainable power system.

Key Elements

Renewables

Flexibility

Grid Structure

Market Design

Challenge Groups

Social Acceptance

Capability

Institutions/Policies

Investment

Entry

Grid Integration

Fossil Industry

Supply Chain

Political Will

The role of the power sector in the energy transition

The power sector transition is a longer process, and depending on each country’s starting point, it may take years if not decades to move from the status quo to achieving the vision. A rapid transformation is however paramount as the power sector plays a critical role for the decarbonisation of other energy intensive sectors.

A swift decarbonisation of the electricity system is essential to achieving economy-wide net-zero emissions, as the transition in other sectors will be based heavily around electrification. Cutting carbon emissions from transport and heat is dependent on the availability of low-carbon electricity, needed to charge electric vehicles, create low-carbon gases such as hydrogen and ammonia, and to power heat pumps in homes. An expected increase in demand for electricity means that a net-zero power sector needs to replace existing carbon-intensive supply with low-carbon alternatives, as well as increasing overall system capacity. Combined with digitalisation, electrification also opens up new opportunities in linking power generation to energy demand and, if well-planned, could help with the system integration of variable renewables.

The power sector is moreover an important pillar of the economy and as such a driver for economic growth and development. Any transition needs to be managed carefully to ensure a just and inclusive process.

The archetype as the conceptual framework to track progress

The archetype provides the basis and framing of the power sector tracking tool and is centred around key challenges to achieve the long-term vision of the sector in its various dimensions. In alignment with the archetype the tracking tool has also been developed from the basis of the key challenges faced in the power sector transition. The challenges were identified through a research process involving all CASE consortium partners, reflecting the country and regional (SEA) perspectives, cross checked against typical challenges encountered in other parts of the world.

Whilst the archetype is a general conceptual framework applicable to all countries, the power sector tracking tool allows for the specific application of the archetype in each country. Building on the different challenge dimensions, the tool defines a set of key indicators against which progress in each of the dimensions can be measured and it can be tracked how close an energy system is to reaching the vision. It can provide a concrete evidence basis to define intervention strategies and activities for CASE and other donor driven programmes as well as policymakers and stakeholders at country and regional level.

General Vision

Key elements of the long term vision

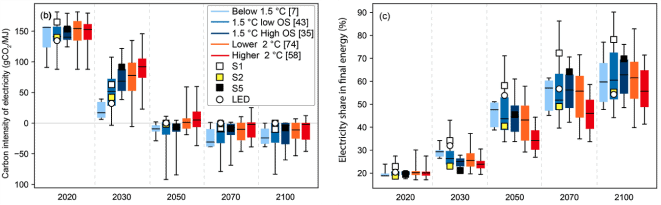

The energy transition in the power sector is a pathway towards a clean, affordable and secure energy system (CASE). The vision ofa clean, affordable and secure energy system entails a net-zero greenhouse gas (GHG) emissions system that is in line with the long term goals of the Paris Agreement which also supports the fulfilment of the sustainable development agenda in terms of social and economic development objectives.

Vision element 1: Renewables

The (future) power system is built around wind and solar

The (future) power system revolves around a combination of wind and solar…

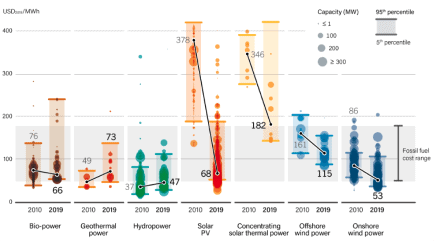

Already cheap and abundant, wind and solar costs are expected to continue to decrease.

… complemented by other renewable and storage technologies…

Hydropower, bioenergy and geothermal are also cost competitive and are poised to play vital roles by providing dispatchable power, other energy services for heating and transport, and other non-energy services (e.g., water storage and flood mitigation by hydropower). Their potential is relatively limited, however, due to concerns around environmental and social impacts or resource availability.

…while other non-renewable options become prohibitively expensive.

LCOEs of new nuclear or fossil-fuels coupled with carbon capture and storage are not cost competitive when compared with renewable energies.

Global levelized cost of electricity (LCOE) from newly commissioned, utility-scale renewable power generation technologies in 2010 and 2019. Fossil-fuel range between 50-177 USD2009 per MWh, lower bound represents new, coal-fired plants in coal-producing regions in China. Source: REN21, 2020 via IRENA, 2020.

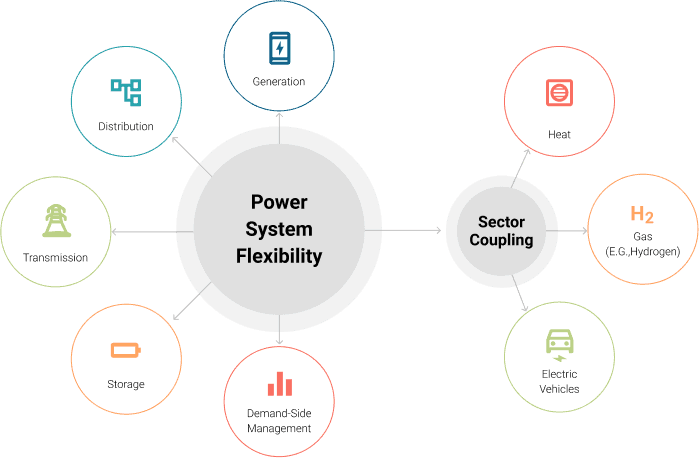

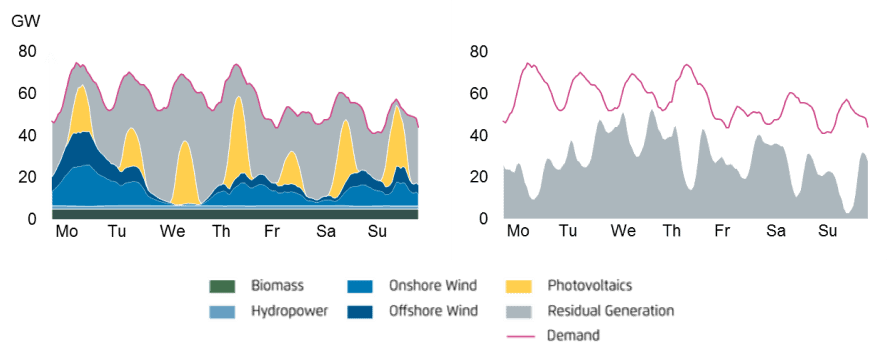

Vision element 2: Flexibility

Power plants, demand and storage are operated flexibly and react to renewables variability

In a power system dominated by wind and solar…

Variable and intermittent by nature, wind and solar will add greater volatility and challenges to instantaneously matching supply with demand.

… system flexibility becomes the new paradigm…

‘Baseload’ operation is obsolete. Generators, storage and demand-sectors that can rapidly adjust operations according to system needs maintain system stability and reliability.

… and will rely on greater interconnectivity between and within power systems.

‘Smart’ sector coupling, e.g., electrification of demand sectors like transport, industry and buildings, will provide new sources of flexibility. Modern and interconnected transmission and distribution grids widen the area in which resources are shared.

Left Top: electricity generation and consumption in a sample week with 50% renewable energy share. Left Bottom: highlighting ‘residual’ generation, i.e., non-renewable generation. Source: Agora, 2016. Right: Enablers of power system flexibility in the energy sector. Source: adapted from IRENA, 2018.

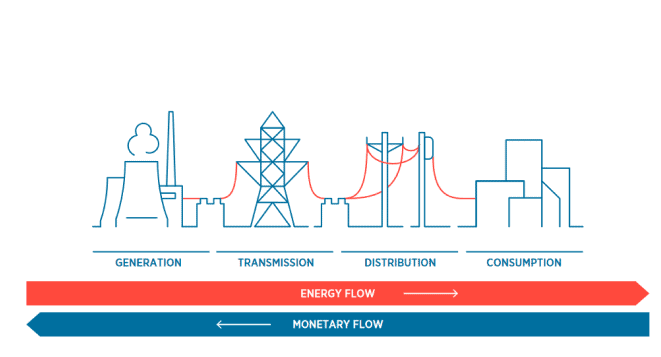

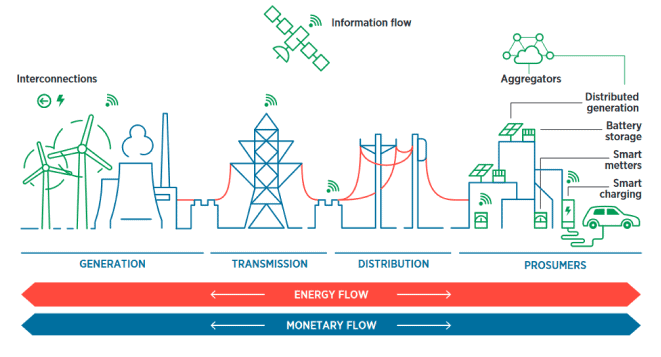

Vision element 3: Grid structure

Relatively simple centralized grid systems evolve into complex decentralized and smart networks

A power system based on renewables focuses on many more small, decentralised structures…

Already cheap and abundant, wind and solar costs are expected to continue to decrease.

… where grids play a more active role in providing flexibility …

Long-distance interconnections and regional power trading enable power to be transported across a wider balancing area, allowing for a greater diversity of resources to balance supply and demand.

… and manage complex bidirectional flows of energy and sector coupling with digital solutions

As decentralized renewables feed into low-voltage distribution grids, transmission and distribution grids become bidirectional. Where power used to flow from major generators to consumers, active energy consumers, or ‘prosumers’, both consume and produce electricity and feed power back into the grid.

The electrification of end-use sectors, e.g., of transport via electric vehicles, or of the heating sector, increases the complexity of the grid system. Digital solutions throughout the grid system help manage the complexity in the new ecosystem of power supply and demand.

Yesterday’s (top) energy supply chain and transmission and distribution grid structures, and the Vision (bottom) with bidirectional flows of energy and money. Digitalisation permeates entire supply chain. Source: IRENA, 2019

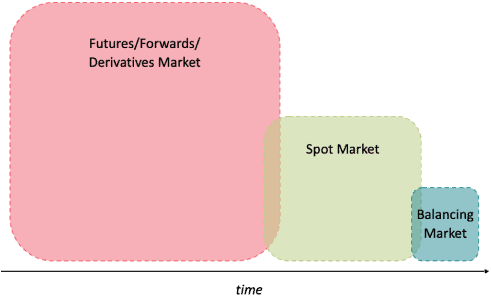

Vision element 4: Market Design

Market and regulatory mechanisms provide necessary signals that ensure the system operates at the lowest cost

In the new renewables-driven paradigm of decentralised resources, flexibility, and smart interconnected grid networks, electricity markets provide the signals needed to ensure system flexibility and long-term capacity investments at the lowest cost.

Although no two market designs are alike, for no two power systems are completely alike, a combination of long- and short-term markets are the basis of a cost-efficient market design:

– Future market: Most power volumes are traded here. The futures market is primarily used for price hedging.

– Spot market: Short-term oriented to level out day-to-day needs.

– Balancing market: Even more short-term, helps to compensate for power and voltage fluctuations in the grid.

Markets are supported by policy and regulatory frameworks where needed and appropriate, for example:

– Financing renewable energies

– Energy efficiency standards

– Long-term infrastructure planning

Illustration of the electricity market, which is made up of various submarkets, each with their own price signals. different markets. Size of square indicates volumes traded. Futures markets can be traded for multiple years into the future, whereas balancing markets happen at a sub-hourly scale.